I talked to a founder recently who’d had a successful exit, when she made an offhand comment: “I’ll never do a deal with liquidation preference again”. It made me realize that most founders I talk to forget one critical financial story: their own. When you’re in the thick of fundraising, it’s natural to assume you’ll make money if you raise capital and have an exit. But that’s not always true!

It’s difficult to get precise data about financial outcomes because deals are private and failures aren’t well-reported. But there are clues. According to a study on angel investing, in 7 out of 10 cases, investors don’t get their money back, let alone make a profit. If outside investors don’t get back capital, founders will walk away with nothing, except possibly their salary – usually not much.

This doesn’t mean you have to resign yourself to misery after years of the grind. But it does mean you have to craft your startup’s growth goal AND funding path to ensure you end up with money in the bank 5-10 years from now.

Three Founders, Three Paths

Here’s a story of three founders who’re all pursuing an opportunity worth hundreds of millions of dollars: new technology that hugely improves diagnostic accuracy. Jane, Jackie and Jennifer, the three founders, all see this, but choose wildly different paths to tap the opportunity.

The Hare

Jane is a healthcare software professional. She develops an AI-enabled diagnostic software for the small hospital where she works. The positive results encourage her to quit her job and start a software consultancy to serve other hospitals. Soon she’s making multiples of her old salary. Hiring a small team of software developers, she easily hits $2 million in revenue in a few years, taking home $700,000 a year. She’s happy running her consulting firm.

The Gazelle

Jackie is a healthcare professional. She sees an intriguing new concept at a conference she attends and immediately sees its applications in her work. She applies and gets accepted at an accelerator. Within weeks she builds an MVP that doctors at her hospital are excited about. With her industry connections she lands three more contracts with local hospitals. She continues pitching in competitions and racks up $150,000 in prize money that’s enough to engage a few talented developers.

Not liking the VC fundraising game, she opts to raise a meaningful angel round with local angels that helps her snag larger regional hospitals and work out the wrinkles in her technology. Three years later, in her annual report to her investors, Jackie confidently forecasts $5 million in revenues, with the ability to hit $10 or even $20 million in 7-10 years.

An acquisition for 2 or 3 times revenue is now a real possibility. A sale for $20 – 50 million means she can take home $15 – $30 million before taxes, because she’s still the majority investor and negotiated good terms for her raise. Her investors would love to fund her next startup too!

The Aspiring Unicorn

Jennifer, meanwhile, sees this as a huge global opportunity. She decides to seek VC funding and raises her first round after months of grueling work, followed by two more quick raises in a favorable market.

With $10 million in the bank, she expands the team, invests in a sales force, and works 80 hour weeks to hit her milestones. Year 2 sales are impressive at $10 million, but fall short of investor targets. She pushes harder. A year goes by, and discussions with the board get tougher.

After 5 years with $20 million in sales, her investors decide to pull the plug on her venture due to slow growth. Shortly thereafter, Tech Crunch announces the acquisition of a competitor for $450 million. She feels like she lost the lottery by a hair.

Decoding the Three Levers In Funding Decisions

These founders made three critical decisions decisions that definitively shaped their payday:

Product and Go-to-Market Strategy:

Your choice of what product you go to market with, and how you’ll sell, have a decisive impact on your funding and payoffs.

- Jane chose to go with a service offering which reduced her risk, but it effectively precluded any option to get external funding for growth. But she generated cash from day one, made a great paycheck, and didn’t need to find investors.

- Jackie sacrificed that cushion by building a product instead of providing services, but earned the option to grow faster and take funding which she took.

- Jennifer made the riskiest bet with a huge payoff, but lost the bet.

Growth-Risk Equation

There is a growth-risk equation – the higher your target growth, the greater the risk of failure. But you get to choose the goal. What you may miss is that this isn’t a binary choice of “lifestyle business” or “unicorn”. Something in between could be your perfect sweet spot for tapping a big opportunity but biting off only what you can chew. Bigger growth aspirations means you’ll need more money – but you may not always need VC money.

Work vs Life Tradeoffs

Investors often say you can either be rich or king (or queen). High growth means you’ll have to sacrifice control and many other (important) things in your life so you can hit the astronomical targets that will appease venture capital investors – that’s just the reality of the model.

The secret is picking a path that will preserve your growth options but still give you the option to pursue control and lifestyle needs. In many sectors and businesses, this is not an all-or-nothing. Lynda Weinman, for example, followed her instincts and the market and eventually sold her “lifestyle” business for $1.5 billion to LinkedIn. ( Follow this link to check out for yourself)

Making Smart Funding Choices for a Better Payday

Here are three strategic steps to make your funding decision pay off for you:

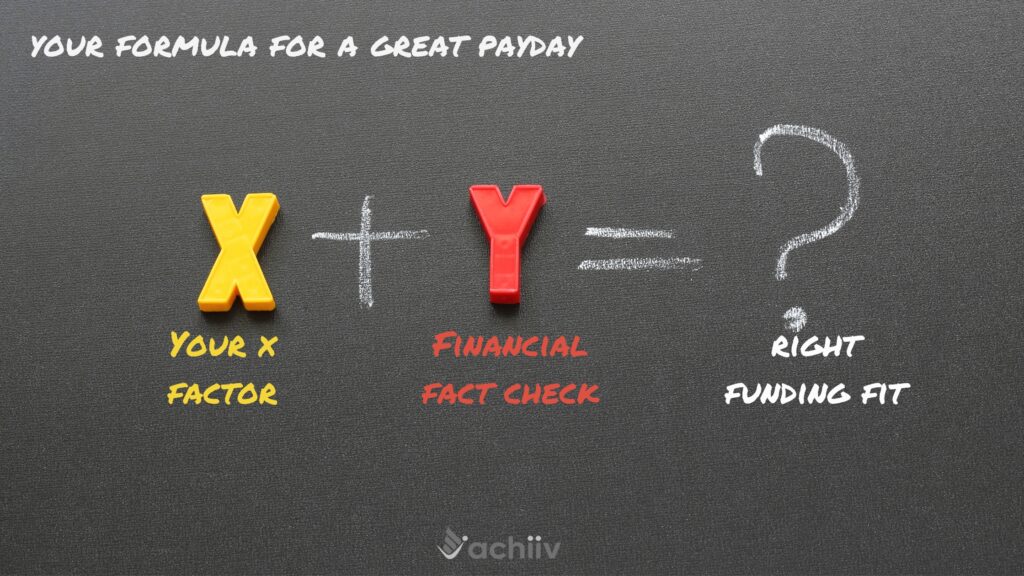

Step 1: Your “X” Factor

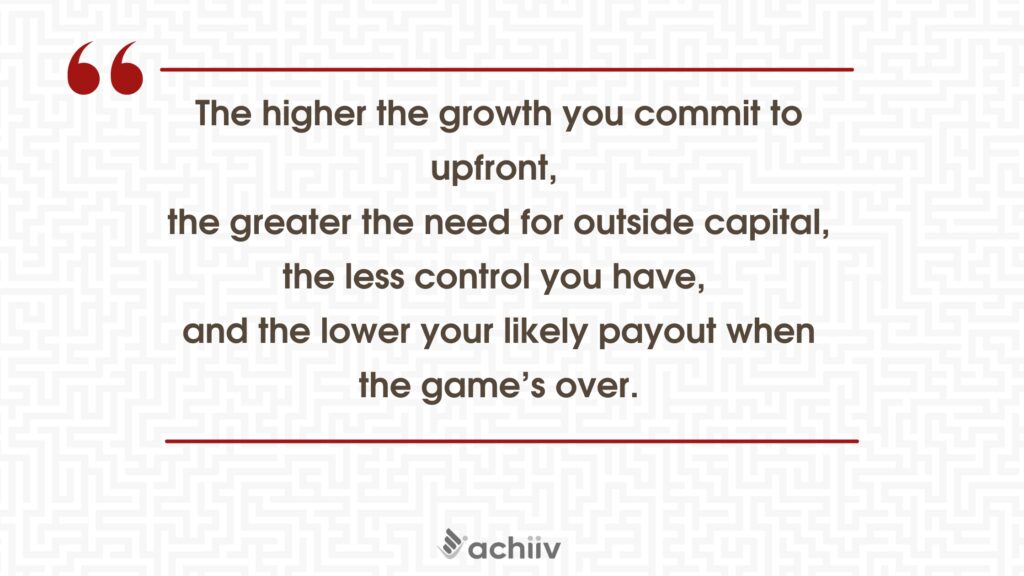

There’s a lens investors use to assess your startup from a growth standpoint: are you a 1X, 10X or a 100X growth startup? A new bakery might be a 1X startup, whereas a software business could be a 1X, 10X or 100X startup. Everything you do to build your startup is downstream from this critical choice. The higher the growth you commit to upfront, the greater the need for outside capital, the less control you have, and the lower your most likely payout when the game’s over. The trick is to see if you can make it work as a 10X company with lower risk while still keeping the growth ceiling and your likely payout high.

Step 2: Your Financial Fact Check

Think through the bare minimum, the ideal and the dream “pots of money” you need or want from undertaking this venture, and the number of years you’re willing to invest to get there. Are you okay with the time/money trade off in the worst case scenario? Founders tend to forget that money is replaceable but the years of your life are not.

If numbers make you uncomfortable, can you paint scenarios of what these look like? For example:

- Worst case – still be able to support your living.

- Ideal case: Never have to work again.

- Dream case: Buy a huge mansion in Hawaii.

Step 3: Funding Fit

For the potential funding sources you’re considering, for example, angel funding, VC funding, self-funding and bootstrapping, consider whether your X factor and your financial fact check align with the funder’s requirements. If you’re going for VC funding, can you realistically commit to the work hours, the loss of control and the ambitious growth these investors require? If not, it’s perfectly okay to walk away from the endless VC pitching to find the funding that works for you.

Putting It To Work for a Bigger Payday

To make this work, start with these four simple questions:

- What do you want your “happily ever after” story to look like for your current startup? What does that mean in terms of size of your company, impact, timing and money?

- What is your current funding path? What are the expectations of these funders? What is likely to be your financial payday on this funding path?

- What is the fit between 1 & 2? How big is the gap?

- If 1 & 2 have nothing in common, what do you need to change? Your growth target, your funding strategy, or both?

What one concrete goal will you set to achieve the payday you want?