In the last post, we saw how to use pattern matching to figure out what your next round requires. This post is about pricing what it actually costs to get there.

This isn’t a trivial question. Particularly in deep tech, your raise size is almost as big a risk as your technology itself. The classic trap: Many founders know approximately what they need to demonstrate at the next stage. They look around at peer companies and market benchmarks for their stage and sector. They define a number that feels “enough” and fits with current trends, and launch their raise.

Six months later, they’re back in front of investors asking for a bridge. Or they’re not back at all.

Of course, your raise size will be influenced by market trends and what peers are raising. But the key factor is whether it’s enough to carry you to your next milestone, a.k.a, your next raise.

The Three Places Founders Get This Wrong

Most founders get this wrong in the same way. They know what they need to demonstrate, but they build the number from the top down: look at what comparable companies raised, pick something in that range, add a buffer that feels conservative. The problem is that what “feels conservative” to founders rarely meets the reality of cash burn.

Specifically, three failure modes come up constantly, and they’re stage-specific in ways most founders don’t realize.

Say you’re building PowerCell, a hypothetical solid-state battery startup raising pre-seed. Your market research tells you that seed investors need a specific cycle life at small scale, a batch production target, and at least one warm automotive relationship.

Budgeting for the Outcome You Want, Not the Uncertainty You Have

Many technical milestones are binary. Your degradation test takes 6 months. If it fails, that’s another 6 months. Most founders budget for one cycle because budgeting for two feels like admitting failure. This optimism bias can cost you the company.

If you fear that this approach makes you look weak, consider whether you have the data to back your optimistic estimate. For example, if you have accelerated test data, prior literature on similar chemistries, or preliminary results that genuinely de-risk the outcome, you can budget for 1.5 cycles, which is one full run plus time to adjust and restart if needed. But without that foundation, you’ll run a serious risk of running out of cash. Being upfront about the rationale will increase your credibility to serious deep-tech investors. They understand the risks.

If possible, break binary milestones into intermediate checkpoints. For example, can you prove 250 cycles in 3 months as a leading indicator before committing to the full 500-cycle test? Decision points beat single pass/fail moments six months out.

Watch out for the mistake of budgeting for one iteration of a pass/fail milestone when you don’t have the data to justify that assumption, only to discover mid-round that you need a second cycle with no cash to run it. Budget for re-runs and multiple trials, not just execution.

Treating “Warm Relationships” as Done Deals

Market validation is the biggest cash sinkhole that traps inexperienced founders. A “warm relationship” with a customer and “pilot commitment” are not the same thing. In battery tech, for example, they might be 18 months and $200K apart because your pilot customer has their own validation protocols, and those protocols cost you money, not them.

The fix is simple but difficult: talking to founders 2-3 years ahead of you, especially to their technical or business development teams, will help you quantify much more accurately the time and money you’ll need to land orders or pilots.

You can also go directly to potential customers without asking for a commitment. What you need from them is a description of their standard validation process. Most will share it because you’re not asking for their proprietary information, only about their process.

Assuming Novel = No Comparables

“Nobody’s built exactly what we’re building” is true for almost every deep tech startup. It does not mean you can’t validate your cost estimates, but it does mean that you have to take a modular, maybe even creative approach to do it.

You can start with component-level quotes. Even if your whole system is novel, the components aren’t. Get quotes from three vendors for each major piece. If you’re building a fusion reactor, you can validate the cost of a specific vacuum chamber and power supply costs, and build up from there.

Then find the adjacent technology. Whoever built the closest thing to what you’re building will tell you if your numbers are order-of-magnitude sane. More importantly, they’ll tell you what always costs more than founders think. For PowerCell, you might talk to a founder who scaled a different battery chemistry, and learn that the scale-up iteration always costs 100-150% more than budget because of some specific technical issue like yield. That one conversation may be sufficient.

The mistakes at this stage are very specific, for example, underestimating non-recurring engineering costs from contract manufacturers who’ve never worked in your category. A manufacturer that knows automotive batteries will quote very differently than one adapting from consumer electronics. Get quotes from someone who’s actually done your type of work.

Finally, show your bottom-up estimate to two or three people who’ve built hardware in adjacent spaces. Ask them what you’re underestimating and what you’re missing entirely. Every single time, they’ll catch something. That’s how your buffer gets allocated to real risks instead of functioning as a vague cushion.

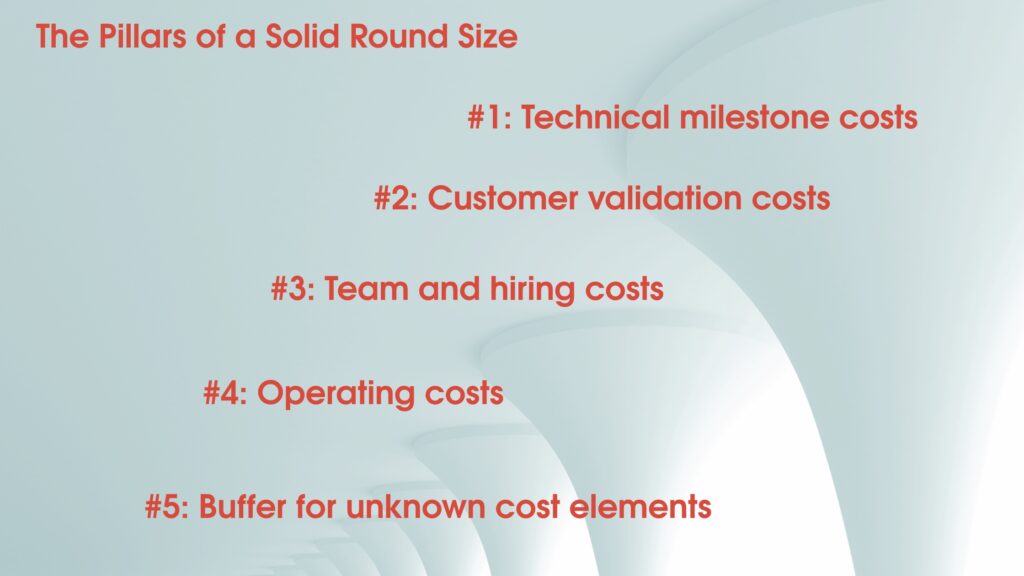

With your bottom up-estimate in hand, you can add 35-40% to your total to arrive at your round size. But that number needs to mean something specific. Your buffer is less of a cushion and more of your honest accounting of what you don’t know yet.

For PowerCell, the buffer might cover the risk of a potential second test if the data doesn’t hold at scale, the gap between your pilot cost estimate and what more customer conversations might reveal, or engineering and manufacturing cost surprises that your experienced advisor warns you about. These are named risks you can reference and support with real dollars, because they come from real facts tied to specific components of your next milestone.

What A Sound Raise Size Looks Like

You know your job is done when you have a line-by-line understanding of the cost components of every milestone you need to hit to succeed at your next raise and priced estimates for each line item from real-world sources.

For example, your PowerCell initial estimate might be $800K (based on looking at comparable raises). After bottom-up costing with vendor quotes and founder conversations, you now revise it to $1.4 million. You understand why: because you underestimated pilot costs by $200K and hadn’t budgeted for iteration.

With this process, your round size is bigger and harder to raise, but your story now becomes:

“We’re raising $1.4 million to demonstrate 500+ cycle life, scale to 100g production, and secure our first automotive pilot — positioning us for a $3-4M seed.”

It’s a much more credible sell and will land better with smart deep tech investors who know the territory and will understand and rate your credibility that much higher.

Before you walk into a pitch, work through this in order:

- What milestones close the gap between where you are and what your next round actually requires?

- What does each milestone cost? Can you back every number with a vendor quote, a supplier price, or a conversation with someone who’s done this work?

- What team gaps must close to execute? What do those people cost over 18-24 months?

- Add it up. Add your buffer. Name what the buffer is covering.

If you can’t answer the second question with actual quotes, you’ve not de-risked your round size. Go get the quotes first.

The round size isn’t a negotiation starting point. It’s the output of clear thinking about what proof costs and what your next investors need to see.

A calibrated round size is also your best insurance against running out of cash and having to raise stressful bridge rounds that are hard to justify and even harder to close.

amlodipine 5 mg

amlodipine 5 mg

viagra price

viagra price

fluconazole over the counter canada

fluconazole over the counter canada